Dr Marko Aunedi, Research Fellow, and Professor Tim Green, Department of Electrical and Electronic Engineering, Imperial College London

16 March 2022

An EnergyREV briefing report is in its final stages of preparation that quantifies the benefits of Smart Local Energy Systems (SLES) in a net-zero electricity system.

This report follows the 2020 briefing paper “Early insights into system impacts of Smart Local Energy Systems”[1], where we first attempted to apply our whole-electricity system modelling framework to evaluate potential system-level benefits of deploying SLES in Great Britain (GB). In our new report we have updated key assumptions, including a shift from a low-carbon (25 g/kWh) to a net-zero carbon system, which also builds on our recent work on viable options for the net-zero GB electricity system[2].

We have assessed the benefits of flexibility through the inclusion of a range of features such as demand side response and energy efficiency of SLES using our modelling framework, the Whole-electricity System Investment Model (WeSIM). We have quantified the system-level cost savings arising from SLES deployment by comparing the system cost in the presence of SLES against a system without SLES (counterfactual). This has included an optimised portfolio of large-scale flexibility assets such as storage, interconnectors and large-scale demand side response but with limited local flexibility. Both the counterfactual and the ‘with SLES’ cases have been constrained to deliver net-zero electricity.

During our modelling we have considered three levels of SLES uptake (Low, Medium and High) and also looked at three counterfactual scenarios (Pessimistic, Central and Optimistic) that differed in the volume of distributed flexibility that is available without any SLES. We have made the assumptions that SLES enhance the uptake of demand-side response (DSR) from electric vehicles (EV), heating, and appliances, wider development of rooftop PV generation and uptake of distributed battery energy storage (additional to EV batteries). The cost of batteries and PV have been accounted for, while for reasons of uncertainty the cost of DSR has not been included. In some studies we also assumed SLES boosted energy efficiency by improving thermal insulation of buildings.

This modelling has provided us with the following insights:

1. Customers involved in SLES schemes who provide DSR are likely to see a reduction in their electricity bills compared to non-SLES customers.

We estimate that in the net-zero GB power system the non-SLES customers would pay around £688 annually for their household electricity (in real 2018 GBP). For an average household this would mean a unit cost of electricity of 11.4 p/kWh.[3] For SLES customers that take advantage of shifting their demand to periods with lower prices, the cost of electricity would drop to £634 annually (about an 8% decrease). This may be an underestimation of the total benefits to SLES customers who can act as prosumers, as it does not include potential revenues from providing flexibility services. These ancillary services include the ability to flexibly respond through certain types of loads such as refrigeration or electric vehicles, or battery storage. However, the annual saving of £54 would need to be set against the cost of enabling the DSR. SLES would bring benefits not only for SLES customers, but also for those outside SLES, as a more flexible and cost-efficient system would also lower the electricity bills of inflexible customers.

2. SLES customer bills savings are fairly robust across various counterfactual and SLES uptake scenarios.

Overall, there is little variation in customer savings between the three counterfactual scenarios. Savings reduce slightly as SLES uptake shifts from Low to High; however, the number of customers enjoying these benefits increases several times. This implies that from the customer perspective there is no substantial difference in savings between early and late adopters of the SLES concept.

3. SLES customers who implement other features such as PV and energy efficiency measures will see further energy bill reductions.

In addition to local flexibility, SLES is also expected to commonly include rooftop PV and energy efficiency measures. With the assumed average deployment of 2 kW of PV capacity per customer, the PV generation would further reduce the cost of bought-in electricity by around 28% (an annual saving of £193 compared to £688 for non-SLES customers), which can be used to offset against the PV investment cost.

Where SLES supports improvements to the thermal energy efficiency of customers’ homes, it was assumed that this would reduce the energy use for heating by 20% compared to non-SLES customers. This would reduce the energy bill further to £401 per year (or 6% reduction on the basis of a non-SLES customer bill). As with DSR, these bill savings need to be offset against the investment cost of PV and energy efficiency, which could potentially result in net costs and not net financial benefits.

4. Deployment of SLES can deliver substantial savings in total system cost.

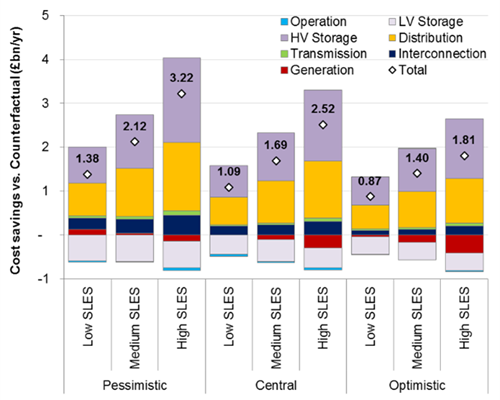

In addition to the impact of SLES on individual electricity bills we also quantified the impact of SLES on total system cost in a net-zero carbon GB electricity system. The economic benefit of SLES is quantified as the difference in total system cost, as found by the model, between a given SLES uptake case and the appropriate counterfactual scenario. Cost-benefits of SLES are disaggregated into (i) investment cost (CAPEX) for generation, network and storage assets, and (ii) operating cost (OPEX) of electricity generation. For Medium SLES deployment and the Central Counterfactual we found that the total system cost savings from SLES were around £1.7bn/yr, or 4.2% of total annualised system cost. As elaborated below and illustrated in Figure 1, the SLES system benefit will vary considerably under different factors and assumptions.

5. The main mechanism for SLES delivering system cost savings is through displacing grid-scale battery storage.

The main opportunity for cost saving is in low-cost DSR facilitated by SLES displacing grid-scale battery storage. The volume of flexibility needed to run a zero-carbon system is relatively constant in terms of capacity, while the split between DSR and battery storage can vary. Another key cost saving is associated with the ability of SLES to provide local flexibility, which helps to avoid local distribution network reinforcement.

6. System benefits of SLES will depend on the level of deployment but also on the volume of flexibility present in the counterfactual.

The cost savings of SLES increase at higher levels of SLES deployment, although there are diminishing returns from increasing the SLES uptake (see Figure 1). As explained above, these benefits are found as the difference in total system cost with and without SLES.

Figure 1. Cost savings of SLES across various uptake levels and counterfactual scenarios

Under the Central counterfactual assumptions, the savings for Low, Medium and High SLES uptake are estimated at £1.1bn, £1.7bn and £2.5bn per year, respectively. We have also found that SLES benefits will be sensitive to how flexible the counterfactual is; system benefits for Medium SLES uptake could increase from £1.7bn to £2.1bn per year in case of a Pessimistic counterfactual, but could reduce to £1.4bn/year with an Optimistic counterfactual.

7. The SLES flexibility mix of DSR and small-scale batteries should adapt to SLES uptake level.

In our studies, the deployment of small-scale, distributed battery storage across residential properties within SLES was cost-optimised for the Low SLES uptake case, where for instance we found that it would be justified to install batteries in about 13% of properties. This battery storage volume was then used as a minimum starting point for Medium and High SLES uptake cases, where the model was allowed to add more distributed battery capacity if cost-efficient. Our analysis has shown that distributed batteries as part of SLES tend to be less cost-effective at high SLES deployment levels, so that at High SLES penetration fewer than 5% of households should have a battery installed. DSR is assumed to be available at a very low cost and is therefore competing against the cost of battery storage, especially at higher SLES uptake levels where the volume of available DSR is also higher. Therefore, if the low voltage (LV) battery capacity was simply proportionally scaled from Low to Medium and High SLES uptake levels, this would be less cost-efficient than the approach where battery volume adapts to SLES penetration. In other words, late adopters of SLES are likely to see a poor business case for including batteries.

8. System benefits of SLES could increase further if they include energy efficiency measures or exclude rooftop PV.

We further studied the impact of the assumption that implementing SLES not only brings enhanced local flexibility but also results in a 20% reduction in demand for space heating due to improved energy efficiency. Using the same approach as before to quantify the system benefit of SLES against a relevant counterfactual scenario, this would further increase the cost savings from SLES by up to £0.6bn/yr (which is additional to the savings already identified for our default assumptions on SLES). However, this benefit needs to be set against the investment needed to implement the efficiency improvements.

Our default assumption was that SLES includes rooftop PV installations, and therefore scaling up SLES results in this additional PV capacity displacing offshore wind capacity, which is actually cheaper according to our assumptions. Removing rooftop PV from SLES therefore resulted in even higher SLES benefits at system level, as it avoided unnecessary generation investment costs. Nevertheless, the value to the SLES investor may be different.

9. Due to significant differences in input assumptions, the net benefits of SLES found for the net zero system are considerably lower than in our 2020 briefing paper.

Our previous “early insights” paper had two principal differences that affected the system benefits of SLES:

- The previous system carbon target was low but not zero-carbon so the system also featured Carbon Capture and Storage (CCS). SLES value therefore mainly came from replacing CCS generation with offshore wind, which does not occur in the net zero system where the counterfactual already features mostly offshore wind and large-scale batteries and contains no CCS.

- Flexibility in the counterfactual was very limited and much lower than what needs to be present in a zero-carbon system with very high renewable capacity. Therefore, the additional flexibility provided by SLES with respect to the counterfactual enabled a higher value due to the ability to displace the cost of CCS.

In conclusion, our whole-system analysis suggests there is a significant potential for local flexibility resources unlocked through SLES to deliver savings in customer bills as well as reduce the cost of decarbonising the energy system. SLES flexibility facilitates changes in electricity consumption patterns that are beneficial for the electricity system due to lower peak demand in local networks, better responsiveness to the availability of bulk renewables such as offshore wind, and reduced need for large-scale flexibility. Although there are challenges related to the implementation of SLES, including governance, markets, customer participation and coordination, the considerable economic benefits of SLES for GB energy system decarbonisation suggest that it would be beneficial to address these challenges in order to fully utilise their potential.

[1] Aunedi, M. and Green, T.C. 2020. Early insights into system impacts of Smart Local Energy Systems.

[2] Aunedi, M. et al. 2021. Net-zero GB electricity: cost-optimal generation and storage mix.

[3] Note that this cost may not fully include the total cost of metering, billing, tax and supplier margins that would also appear in a retail price, and should therefore only be considered as benchmark for various scenarios of SLES uptake.