By Fabian Fuentes Gonzalez, Jan Webb, Maria Sharmina, and Matthew Hannon - EnergyREV Business and Financial Practices team

The EnergyREV Business and Financial Practices team has compiled a database of companies involved in the energy business and finance sector in the UK. Many of these businesses meet some of the characteristics that define a Smart Local Energy System (SLES). In general, their level of indebtedness seems appropriate in the context of energy markets, even though further analysis is necessary.

The world is changing and bringing uncertainty at lightning speed, nowhere more so than within the energy sector. There are significant opportunities and challenges associated with net zero carbon targets, digital technologies, innovative thinking, and renewed interaction between energy companies, citizens and policy makers. SLES represent an opportunity to challenge the UK history of centralised, large-scale fossil fuel systems and markets, contributing to decarbonising, decentralising, digitalising, and democratising energy.

The EnergyREV Business and Financial Practices team has created a local energy business database, bringing together many sources of publicly available information. This database will help us to better understand local energy businesses involved in SLES and their financial situation, in order to inform next-generation business models and potential financing for integrated systems.

Our database contains 699 energy businesses, including aggregator services, equipment (heat interface units) maintenance, supply of electricity for EV charging, and cooling. One interesting example is a pumped storage power station in Snowdonia (North Wales) which has established a visitor centre with tourist facilities and tours inside the power station. There are also entities involved in energy and waste management services, which have agreements with local authorities to manage/recycle different kinds of waste (food, solids, liquids, and even packaged goods) as part of energy generation; some of them have specific funds for communities. The sample included in our database gives a rich and representative picture of the current UK market, with some businesses closer to a SLES than others. The database uses the financial, legal, and commercial information provided by Bureau van Dijk through its product [1], a time series database of UK and Ireland businesses. We extended the FAME data by integrating information from company websites, publicly available notes to the financial statements, media articles, and other public sources. This extra information includes the number of customers, revenue streams/sources, technologies and installed capacity, provision of benefits to communities, and ownership.

We have found that most businesses in the sample are privately owned (78%), but there are others that take the form of community interest companies (6%) - a type of limited company conceived to benefit communities rather than shareholders - and others owned by trusts, foundations or community groups (13%). Councils and universities own the remainder (3%).

If Companies House thresholds based on (average) assets or company resources are used as a way of calculating company size, we notice a fairly even distribution: 8% can be categorised as micro (typically with one employee), 48% as small (typically one employee), 29% as medium (typically five employees), and 15% as large (typically 37 employees).

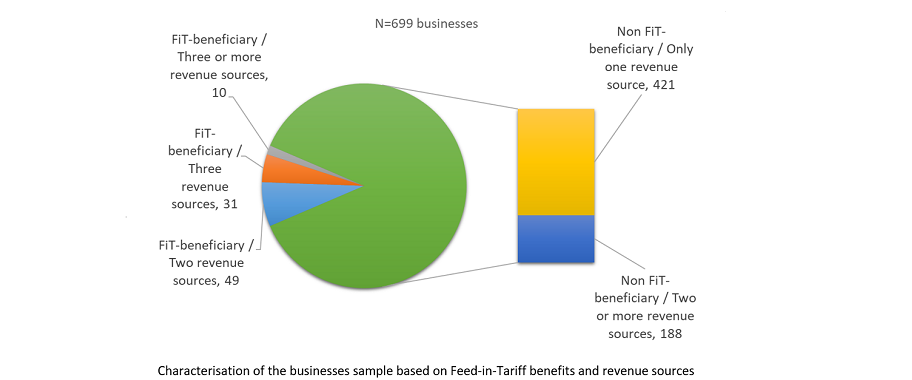

Knowing the revenue sources of companies allows us to better understand their core businesses and, therefore, how they generate their income. Most of the businesses within the sample (421 out of 699) have only one revenue source, which is mainly sales of electricity to the grid (276 out of 421) using renewable sources and technologies, for instance, solar PV, wind or hydro. On the other hand, just over a quarter (188 out of 699) have two or more revenue sources, including production of bio-fertiliser, food waste management, injection of gas into the grid, heat and power services, power purchase agreements (PPA), financial lending to related companies, gain on investments, and Renewable Obligation Certificates (ROC).

There are also businesses receiving public subsidies almost 13% of the businesses (90 out of 699) declare receipt of Feed-in-Tariff (FiT) benefits; most of these have two (49) or three (31) revenue sources. This gives a general idea about the companies’ dependence on public resources to carry out their business activities.

All businesses can be funded with equity and/or debt. One key financial indicator is the debt-to-equity (D/E) ratio, which is simply a coefficient derived from items in the financial statements. This indicator is important because it indicates how companies finance their operations and their ability to cover debts with shareholders’ funds in case of downturn. Beyond having a referential value or threshold for this indicator, an accurate interpretation of it should also consider the context of the industry where the businesses under analysis are[2]. From 2010 to 2018, for businesses in our database, those in private ownership have a ratio between 1.4 and 2.3. This means that companies’ debt is between 1.4 and 2.3 times shareholders’ funds. Businesses owned by universities had a higher ratio of 2.5 on average from 2010 to 2012, followed by a continuous drop to 0.8 in 2018. Businesses owned by trusts/foundations/communities show even higher ratios of debt to equity, with an average of around 2.8 from 2010 to 2012 and nearly 4.0 from 2013 to 2018. Municipally owned businesses show negative values for equity most of the time, and their liabilities (current and long-term) reach circa £14 million on average. Similarly, most of the community interested companies had negative values for equity during the years analysed, and their liabilities reach an average of £1.6 million; this implies a very high average D/E ratio (12.8), due to the inclusion of companies with negative equity. In general, the level of indebtedness seems to be within the standard of the energy services industry, but further analysis is necessary.

Some businesses are closer to a SLES than others. For example, some organisations are already involved in areas of SLES value creation[3], such as providing energy services which combine heat and power, enhancing environmental eco-system benefits beyond carbon reductions (e.g. waste management and biofertilisers), social justice and energy equity (e.g. community funds/grants), and social needs (e.g. employment, education, and even leisure). However, most current businesses appear to be struggling with ‘smartness’, including the adoption of real time information technologies; rapid, flexible response to changes in energy demand; use of machine learning or artificial intelligence, and engagement with stakeholders in planning, decision-making and governance. Concerning localness, some businesses are involved with communities through providing defined benefits and/or third sector or public ownership. We are now doing further work to explore which companies are closer to the SLES model.

These brief comments deliver context and insights into companies’ performance and ability to create value, and then invest in other energy activities to provide smart local services. Our work continues with more detailed analysis of the data for future reports. This new business and financial knowledge will support innovations for a more decentralised, clean, affordable, resilient and democratic, energy system in the UK.

[1] The University of Edinburgh licence.

[2] The standard level of debt-to-equity can vary from one industry to another. One example of high debt-to-equity (D/E) ratios is the financial services industry. Having high levels of debt could imply a high exposure to financial risks (for example, interest rate fluctuations) but companies can mitigate them through different measures.

[3] Ford, R., Maidment, C., Fell, M., Vigurs, C., and Morris, R. 2019. A framework for understanding and conceptualising smart local energy systems. EnergyREV, Strathclyde, UK. University of Strathclyde Publishing, UK. ISBN: 978-1-909522-57-2